Is money social? And how?

Earlier this year we discussed financial decision making and emotions, arguing that the average decision maker is quite different from “the economic man”.

And just like the tendency to assume humans to be rational, while really they are not, there is a tendency to identify the economic or financial unit as an individual–when in fact it could be a family or a community.

So, how is money social –and how do we provide financial solutions to serve social money issues?

People may often want to make economic or financial decisions with a partner (like buying a home), a family (general spending or savings) or in some matters with a group of friends (like saving for a holiday). And even when financial decisions are made by an individual, they may certainly affect many people–like a whole family, children, friends, or the local community.

From a different perspective, we also know that people look for financial advice from people they trust–often family and friends. We often assume that taking financial action, such as investing money, begins with thinking about it and ends with actually creating a fund or an account, or buying stocks and bonds. In reality, however, it probably takes much longer, since most of us would want to know about other people about their experience with banks and apps, or approach close friends and family about the risk of loss. And even if these people were not professional financial advisers, we would value their word.

Since many people seek this kind of social advice in the age of digital communication and social media we are seeing a rise in people offering it. Just like you may trust the rating of a particular online shop, you may look for the views of a particular investment community, like Female Invest, or a particularly trustworthy person. We will be diving deeper into the whole phenomenon of “finfluencers”, like Queenie Tan, in a separate blog later.

So, how do we develop financial solutions that recognize the consumer as a social being?

Historically there are many examples. Savings and loan circles are well known among people who are not served by traditional banks and financial service providers. To this day, these are common both in poor regions of the world and in poorer communities in richer parts of the world. Generally, group members contribute a small amount of money towards savings on a regular basis, for instance weekly. The group keeps books and members can take turns to take out savings or even loans. These types of alternative financial solutions have different names and structures in different parts of the world. They are however also becoming digitally supported. See for instance the Savings Group Information Exchange for statistics.

Basically, cooperative banks operate in a fashion similar to savings and loan circles–though regulated. Many cooperative banks were created precisely to cater to communities not traditionally served by commercial banks. Often owned by the customers themselves, they would provide saving opportunities and mortgages as well as funding for small businesses, small holders and cooperative businesses. In the insurance industry, mutual insurance companies were founded by policy owners to cover member’s risks. There are many sources to the history and present status on cooperative finance (see, for example, European Association of Cooperative Banks or the World Banks Center for Excellence for Cooperative Financial Institutions).

About ten years ago I was part of an organization hosting the world’s first “startup weekend” with the theme of finance. We expected to see many proposals of payment apps and devices–and so we did. But participants also produced around five ideas to build different kinds of internet-based savings and funding solutions to help finance community needs– roads, schools, art, and so on, all in local areas. Many of the young people were a little surprised to learn that the idea of cooperative banks already existed. A situation that makes you want to know what would come of bringing these tech savvy young people in contact with cooperative financial managers.

Of course, crowdfunding is another example of a peer-to-peer solution. Donation-based crowdfunding is social in the sense that it brings together many people to support a specific cause. Crowdfunding of business projects–big or small–is a way of supporting new solutions with relatively small amounts of money. At the same time it allows companies to raise money as well as get an impression of customer interest in their product. This market is valued at 12,2 bill US dollars and growing fast.

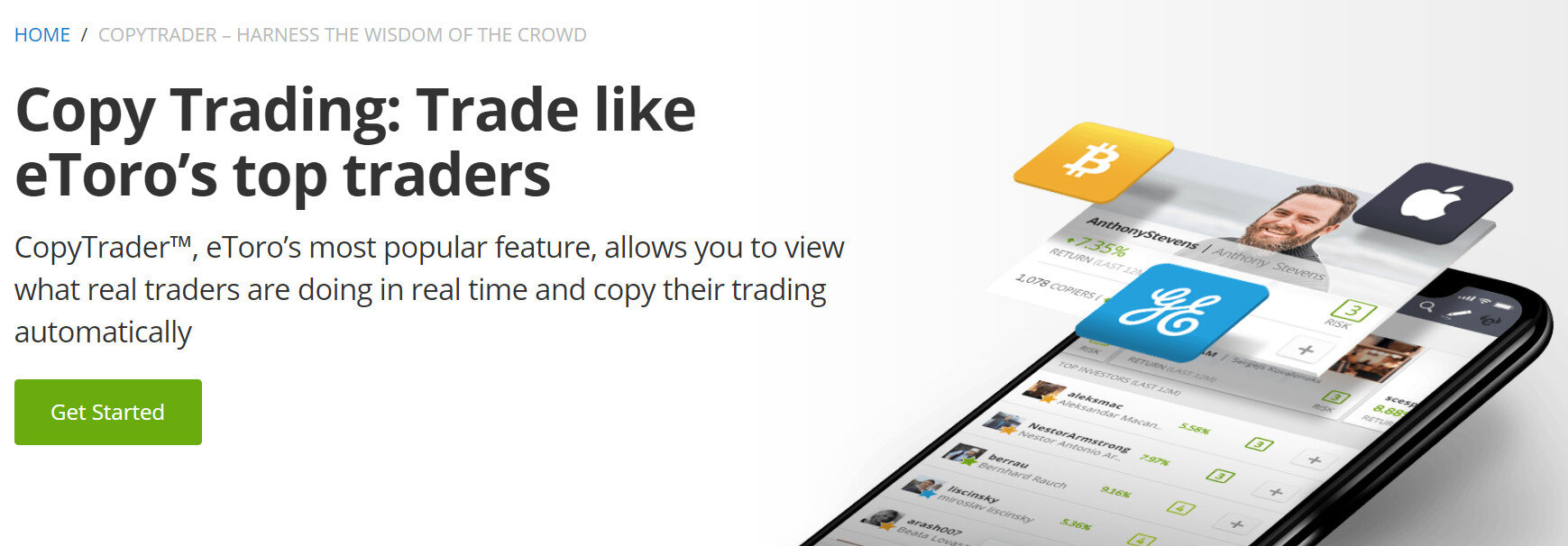

Over the last few years we have increasingly seen the emergence of socially based investment solutions. Some internet-based investment solutions, like eToro, provide the possibility to follow and learn from other investors who are willing to share their buying and selling decisions.

An app like Voleo provides a solution to choose or build an investment community (for example with your friends or family), invest together, follow your progress, and benchmark against the results of other groups.

And as we have seen from our work with financial solutions for women, an increasing number of investing networks are forming. They allow people (and particularly women) to discuss investment profiles, expectations and results, as well as to partake in educational initiatives and events to learn more about investment and risk management.

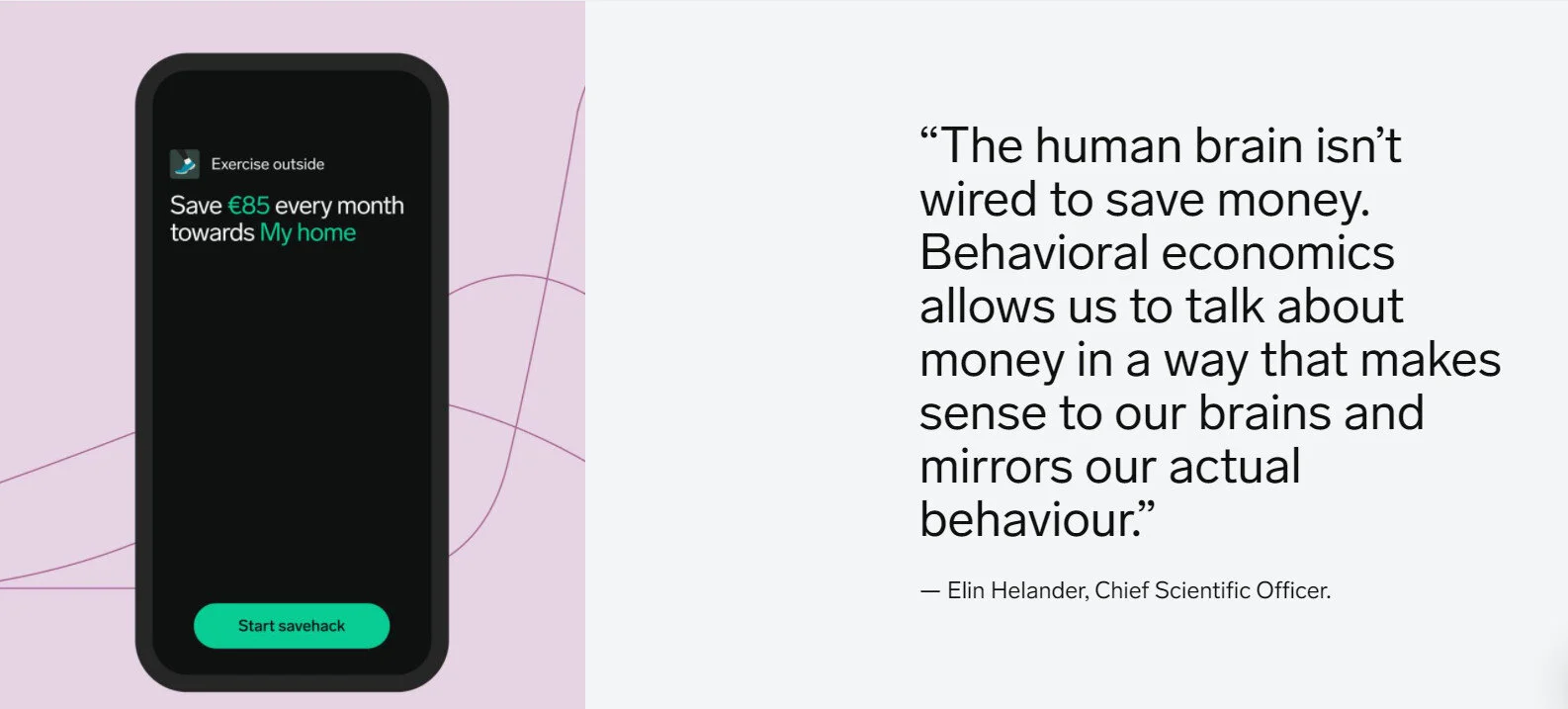

Something similar is developing with regard to daily savings and spending. About ten years ago I had the opportunity to host an event led by a Danish design company. We had invited about 70 people with some connection to finance to be part of an experience to develop new financial solutions. When the different groups shared their results, most were proposing social solutions. To save toward a particular goal–say a holiday–sharing progress on Facebook. To save or invest with other people–say a group of friends. To follow your results on your phone. And to be able to share your results or compete on Facebook. Of course, most of these solutions are widely available now from fintechs such as Dreams or Nav.it.

So, the answers to the questions in the title of this blog are definitely ‘Yes’. Money and finances are social. While many people may not share the details of their income or wealth they may very much seek the opinion of trusted friends or internet sources for advice on their choice of bank or mortgage, or just which payment app is the best. Further, many financial choices–such as buying a home–are actually made by more than one person and for more than one person. And lastly, new ages and new technologies seem to invent new solutions for community initiatives.

Certainly, there is a balance to be struck between focusing on an individual’s economic and financial situation versus, let’s say, that of a family. In times when relationships form and change, it is important to discuss how savings and expenses should be managed with a view to both short-term decisions and long-term issues like retirement.

Earlier times saw women left in a very poor financial situation in case of a divorce if she had neither an education nor job experience or savings. Today we increasingly see examples of young couples partnering in house, mortgage and children without discussing how this should best be handled economically and financially over time. It is very good to share expenses equally, but what happens if both partners' incomes are very different, or if one partner stays at home for some time to take care of children? And how different will their retirement prospects look? Bank Cler in Switzerland did a great report on these issues just last year.

Money matters are always social, and it is a mistake to assume that financial decisions are (or should always be) made by individuals. We have always catered to the social nature of money. While financial service providers sometimes seem to forget this, it’s great to see that fintech innovators and designers keep rediscovering it and coming up with new social solutions and advice for money–whether they know the history or not.